S2F Tools

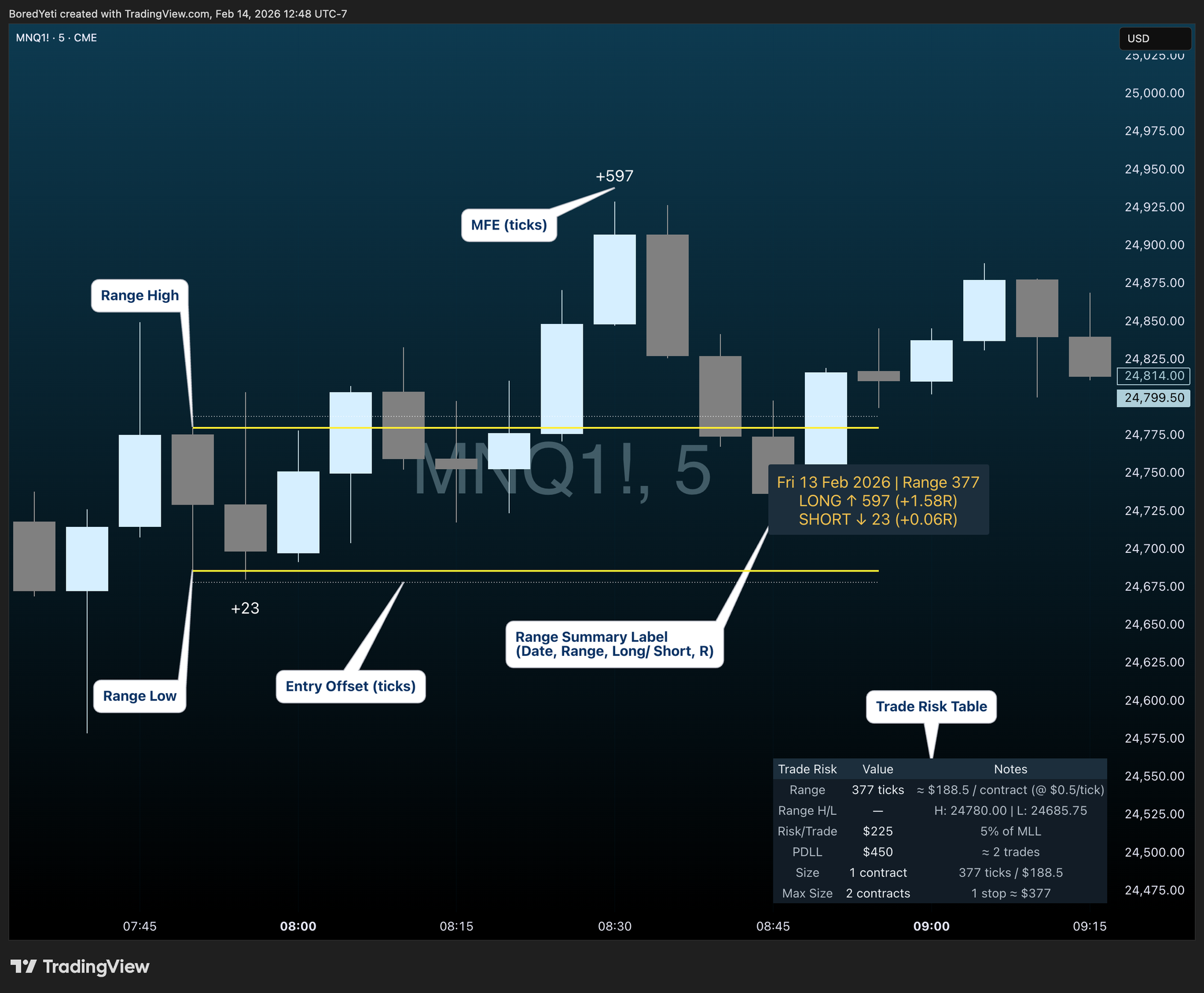

The S2F Futures Risk Manager turns each session range into a consistent reference you can review across days and instruments. It plots the range high/low, prints a summary label, and marks post-range follow-through (MFE) so you can compare outcomes without manual measuring. The trade risk table converts the current range into ticks → dollars → contracts, helping you size positions based on volatility and your risk limits.

- Range structure: Plots Range High/Low and keeps the chart clean and consistent.

- Entry planning: Optional offset trigger lines for staging breakout entries above/below the range.

- MFE tracking: Prints post-range excursion as a simple number so you can gauge follow-through.

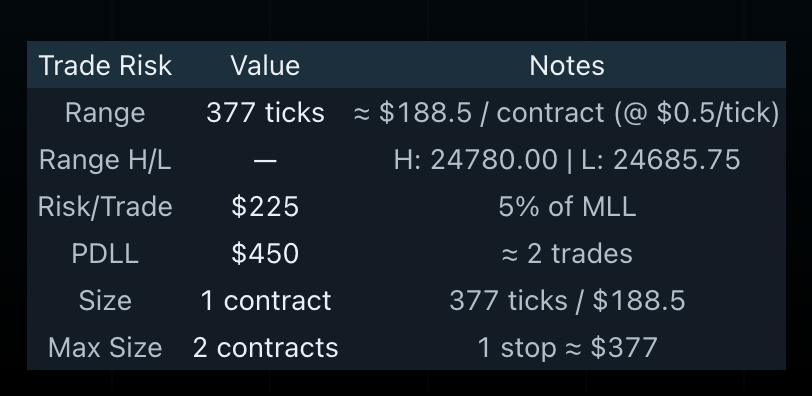

- Risk table: Shows $/tick and estimated $/contract impact for the current range, then calculates Risk/Trade, PDLL, and contract size.

- Research-friendly: “Keep Last N” lets you scan recent ranges and outcomes without clutter.

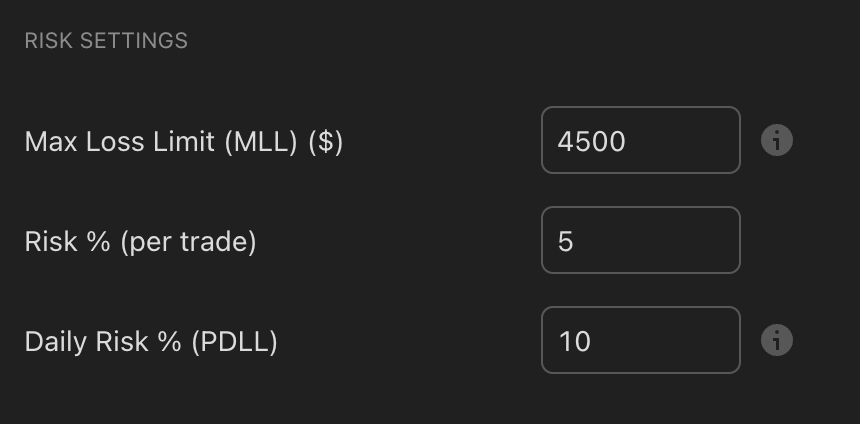

Example: MLL $4,500 × 5% = $225 Risk/Trade. MLL $4,500 × 10% = $450 PDLL.

The S2F Futures Risk Manager table is built to remove guesswork from sizing. It shows the contract’s $/tick, converts the current range into an estimated $/contract risk (based on the opposite-side stop), then calculates Risk/Trade from your MLL and risk %. From there it returns a contract size for current conditions and prints PDLL so you can see your daily loss cap and roughly how many full-risk attempts fit inside it.

- $/tick + $/contract context: Shows the tick value and the estimated per-contract risk for the current range.

- Range → dollars: Converts today’s range size into a dollar number.

- Position size: Calculates estimated contracts from your Risk/Trade and the range-based $/contract risk.

- PDLL guardrail: Displays PDLL ($) and an estimate of how many full-risk trades fit inside it.

- Table controls: Position, text size, colors, and row toggles so you only keep what you use on screen.

This is useful for prop and personal accounts because it ties size to your risk limits, not to a fixed contract count.